Note on the data: All figures are from Zepto’s Draft Prospectus (DRHP) dated June 8, 2026, shown in ₹ millions for the financial year (FY) ending March 31. This is an educational analysis, not investment advice. Bonus: Download our complete Excel model, research report, and investment memo below.

Download the Zepto Financial Model, Research Report and the Investment Memo

Introduction

Can you actually build a highly profitable, massive business by delivering a packet of coffee and a tub of ice cream to someone’s door in under ten minutes? That is the multi-billion-dollar question behind the Zepto IPO.

In less than five years, Zepto has scaled from a pandemic-era experiment by two teenage college dropouts into one of India’s most valuable private internet companies. Now, it is filing to go public through the Zepto IPO, asking everyday retail investors to buy into the quick-commerce dream.

But behind the spectacular growth headlines lies a harsh reality:

the company currently loses a quarter of every rupee it brings in.

This guide takes a clinical, analyst-style look through Zepto’s updated Draft Red Herring Prospectus (DRHP) dated June 2026.

In this, we will strip away the marketing hype and look at the raw mechanics of the business: where the money comes from, how a “dark store” breaks even, who is cashing out, and the metrics that will decide whether this Zepto IPO is a long-term wealth creator or a capital destroyer.

Comprehensive Summary: Key Zepto IPO Details at a Glance

- What is Zepto: Zepto is a quick commerce grocery delivery platform built around the idea of delivering everyday essentials, from groceries to electronics, to a customer’s door in under ten minutes. It was founded by Aadit Palicha and Kaivalya Vohra and has become one of India’s most valuable private internet companies in under five years.

- About the Zepto IPO: It marks the company’s move from a privately held startup backed by venture investors to a publicly listed company on Indian stock exchanges, opening the business up to retail investors for the first time.

- Zepto IPO Launch Date: The DRHP that forms the basis of this analysis is dated June 8, 2026, and while the final Zepto IPO date for listing will depend on regulatory approvals, the filing itself signals that the public offer process is now firmly underway.

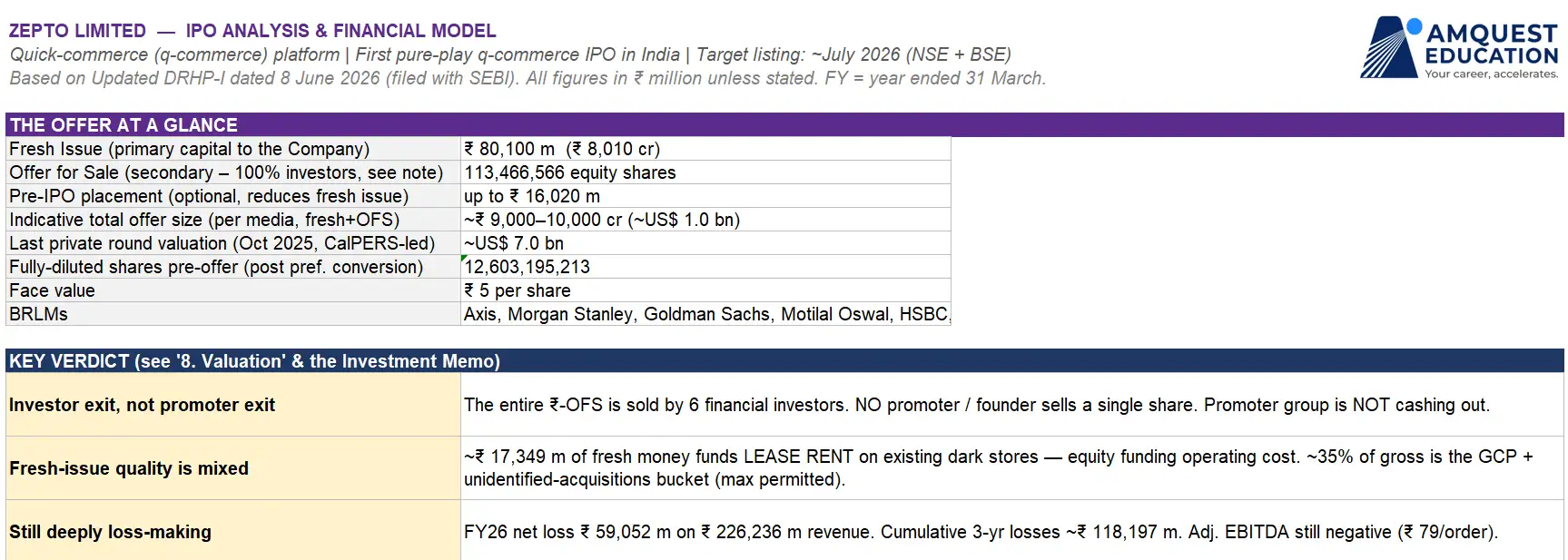

- Zepto IPO Issue Size: It is made up of a fresh issue of ₹80,100 million in new shares plus an offer for sale of 113,466,566 existing shares from early investors, none of which belong to the founders.

- Zepto IPO Valuation: Anchored to the company’s last private funding round at ₹37.74 per share, the valuation of it is then roughly ₹475,645 million, or about US$5.6 billion, on a fully diluted basis.

Key Takeaways

- Zepto features explosive revenue growth but remains deeply unprofitable, losing roughly ₹79 on every order it fulfils despite doubling its scale year-on-year.

- The recent improvement in unit economics was heavily driven by an 87% cut in digital marketing spend right before the Zepto IPO, a lever that may be impossible to maintain as giants like Amazon and Flipkart enter the space.

- High-margin advertising revenue, not grocery sales, is the true engine driving the platform toward a sustainable path to profitability.

- Using permanent equity from the fresh Zepto IPO issue to fund recurring dark store rent obligations signals that capital is being used to offset ongoing operational burn rather than pure growth asset creation.

- The company’s most recent private funding round provides a concrete valuation anchor of ₹37.74 per share, meaning any IPO pricing above this level leaves retail investors with very little margin of safety.

- Taken together, these signals matter most for anyone deciding whether to subscribe to the Zepto IPO once the price band is announced.

01 · THE PITCH, AND THE CATCH

Groceries in Ten Minutes, Zepto IPO Losses in Nine Figures

Order a packet of coffee, a phone charger and a tub of ice cream at 11 p.m., and a rider is at your door before the kettle boils.

That is the promise that took Zepto from a lockdown experiment by two college dropouts to one of India’s most valuable private companies in under five years.

The founders, Aadit Palicha and Kaivalya Vohra, are still in their early twenties.

The company they built now files to go public through the Zepto IPO, asking the Indian retail investor to buy in.

Here is the catch the headlines tend to skip: the faster Zepto grows, the more money it loses.

In the year to March 2026, it booked revenue of ₹226,236 million, more than double the year before, and still reported a net loss of ₹59,052 million.

That is roughly a quarter of every rupee of revenue, vanishing.

The prospectus is, in effect, two documents bound together: a genuinely spectacular growth story, and a genuinely unresolved profitability question.

The business doubles every year. So does the case for and against owning it.

The rest of this piece takes the prospectus apart the way an analyst would:

- The machine

- The money in

- The money out

- The unit economics

- The rivals

- The cap table

- The governance

- And finally, the valuation

And translates each into plain language. Where the disclosure hides something important behind an accounting choice or a defined term, that is flagged.

Want to master IPO analysis?

02 · THE MACHINE

How a “Dark Store” Actually Pays for Itself

Zepto does not run shops you can walk into. It runs “dark stores”, small, windowless micro-warehouses, each stocking a few thousand of the fastest-moving items, placed deep inside dense neighbourhoods so that almost every order is a two-to-three-kilometre dash.

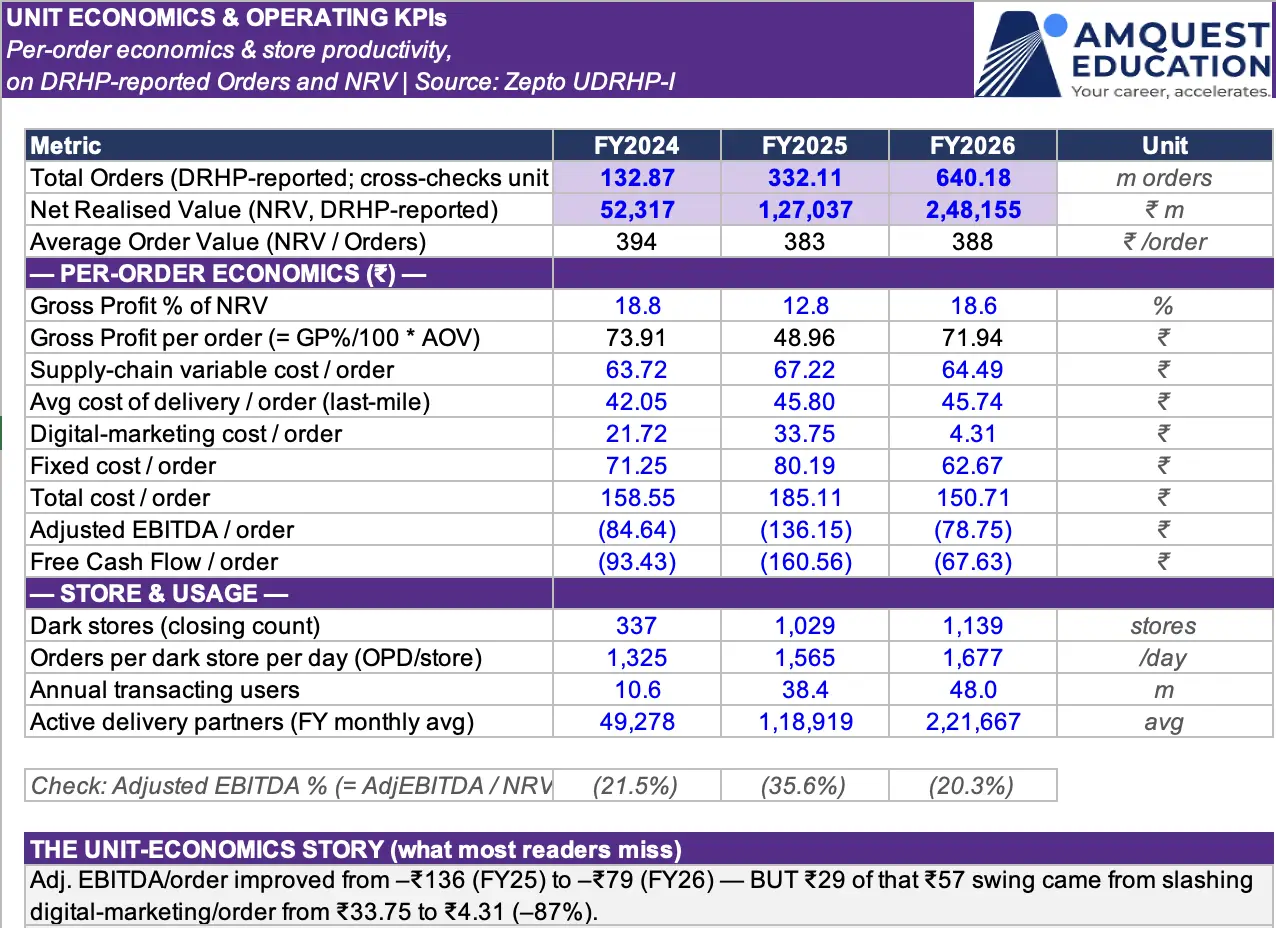

As of March 2026, there were 1,139 of them.

The genius and the curse of the model both live in one number: orders per store per day.

A dark store has a largely fixed cost, including rent, the staff who pick and pack, the electricity, and the shelving.

Whether it fulfils 800 orders a day or 1,800, that base cost barely moves. So the entire game is cramming more orders through each store.

Zepto now averages 1,677 orders per store per day, up from 1,325 two years earlier. Every extra order spreads the same fixed cost over a larger base; this is the “density flywheel,” and it is the single most important idea in quick commerce.

Understanding this density flywheel is essential context for anyone evaluating the Zepto IPO.

Why This Is a Metro Game (and a Constraint, Not Just a Strength)

Density only exists where people are packed together.

The model works in high-density urban pockets, the big metros and a handful of tier-1 cities, where enough orders cluster within a 10-minute ride of one store.

The prospectus is candid that expansion into lower-density towns is structurally harder, which effectively caps the addressable market at India’s denser cities.

The read-through: Zepto’s growth runway is real but geographically narrower than “one-billion-Indians” rhetoric suggests, and the most lucrative metros are exactly where every rival is also fighting hardest, a dynamic that will shape demand long after the Zepto IPO.

03 · FOLLOW THE MONEY IN

Four Revenue Streams, and a Fifth That Quietly Does the Heavy Lifting

Zepto earns money in four visible ways:

- A commission on the goods sold through its platform

- The delivery and handling fees users pay

- The income from its wholesale procurement-and-distribution arm

- And, increasingly, advertising

That last one matters more than its size suggests.

Advertising is the hidden engine. Brands pay to appear at the top of your search for “chips” or “shampoo.”

That money is almost pure margin; there is no cost of goods behind it.

Ad revenue reached ₹16,357 million in FY26, up 151% in a year and more than thirty times its FY24 level, and now equals 7.78% of the value of everything sold on the platform.

In a business that loses money on the groceries themselves, advertising is the most profitable rupee Zepto earns, and the clearest route to the bottom line turning black.

This advertising engine is one of the numbers prospective Zepto IPO investors are watching most closely.

Want to build expertise in IPO analysis?

A Number That Looks Bigger Than It Is

Zepto’s “revenue” is booked gross.

Because Zepto largely takes the goods onto its own books, its reported revenue (₹226,236 m) is very close to the total value of goods sold across the platform, its “Net Receivables Value” of ₹248,155 m.

Many readers will compare this revenue against rivals and conclude Zepto is far larger. It is not necessarily so.

Why it matters: a gross-revenue company and a net/commission-revenue company are not comparable on a revenue line at all.

The honest way to size these businesses against each other is orders and value-of-goods-sold, never headline revenue, a distinction every Zepto IPO investor should keep in mind.

04 · FOLLOW THE MONEY OUT

Where ₹290 Billion of Costs Actually Go

Against ₹231,284 million of total income, Zepto spent ₹290,267 million in FY26. The shape of that spending tells you what kind of company this is. Four lines dominate:

| FY2026 expense | ₹ million | What it is |

| Purchase of traded goods | 184,850 | The groceries themselves, ~64% of all costs |

| Delivery & handling | 30,463 | Paying the riders: the last-mile |

| Other expenses | 48,383 | Tech, cloud, marketing, rent, admin |

| Employee benefits | 17,847 | Staff and stock-based pay |

| Depreciation & amortisation | 8,943 | Mostly leased-store assets |

| Finance costs | 2,648 | Largely lease interest, not bank debt |

The takeaway is that Zepto is, at its core, a thin-margin retailer with a logistics layer bolted on. Two-thirds of the cost base is simply the wholesale price of what it sells. The money is not lost to extravagance; it is lost to the structural reality that selling groceries cheaply, picking them by hand and racing them across a city in ten minutes is expensive, and Zepto, for now, charges customers less than all of that costs. These cost lines form the backbone of the financial picture behind the Zepto IPO.

The burn, in cash terms: the business consumed ₹34,624 million of operating cash in FY26, an improvement on the ₹46,248 million it burned the year before, but still a serious drain.

It carries no bank debt; it is funded by equity and by stretching its suppliers (trade payables stood at ₹37,248 million).

And its accumulated losses have eaten into its capital: net worth fell from ₹61,478 million to ₹35,596 million in a single year, a return on net worth of minus 166%.

05 · THE UNIT-ECONOMICS STORY

It Loses About ₹79 on Every Order, and Part of the “Improvement” Was Bought, Not Earned

Strip the company down to a single order, and you see the truth most clearly. On an adjusted-EBITDA basis, Zepto loses roughly ₹79 on every order it fulfils. The encouraging news is that the figure improved sharply, from a loss of about ₹136 per order in FY25 to ₹79 in FY26. The uncomfortable news is how.

Roughly ₹29 of the ₹57-per-order improvement came not from the business getting more efficient, but from spending far less on marketing.

Zepto cut its digital-marketing cost per order by about 87%, from roughly ₹34 to barely ₹4, in a single year. That is a legitimate lever, and it signals confidence that customers now come back on their own. But it is also the easiest lever in the business to pull just before an IPO, and the first one a price war forces you to abandon.

A genuine, durable path to profit has to come from the supply chain and from advertising, not from quietly switching off the customer-acquisition tap. Watch whether the per-order loss keeps shrinking once competition heats again, a trend that will be closely tracked once the Zepto IPO is live.

06 · THE COMPETITION

The Quiet Leader, the Slipping Challenger, and the Giants at the Gate

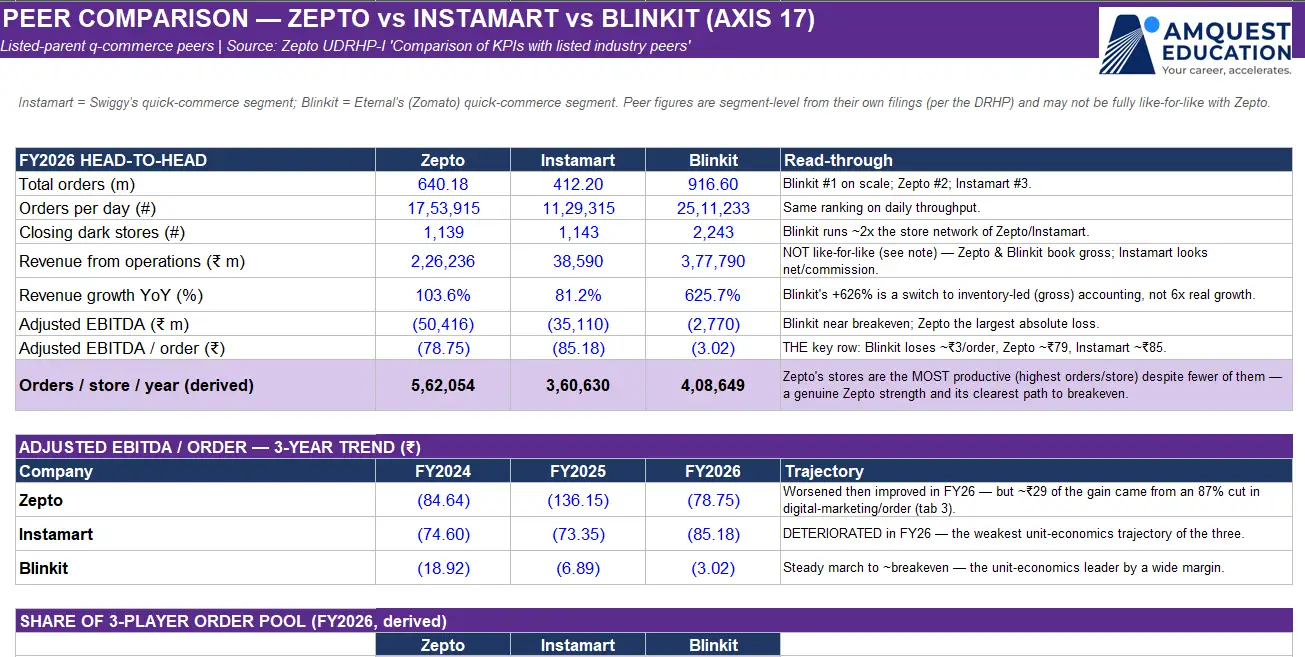

Zepto is not the biggest player, and on the metric that matters most, it is not the best. The prospectus’s own peer table, comparing the three scaled platforms, is unusually revealing. Here’s how Zepto stacks up against these rivals is at the heart of the investment case for the Zepto IPO:

| FY2026 | Zepto | Instamart | Blinkit |

| Total orders (m) | 640 | 412 | 917 |

| Dark stores (#) | 1,139 | 1,143 | 2,243 |

| Orders / store / year | ~562,000 | ~361,000 | ~409,000 |

| Adj. EBITDA / order (₹) | (78.75) | (85.18) | (3.02) |

| Share of these 3 (orders) | ~33% | ~21% | ~47% |

Read the fourth row twice. Blinkit, owned by the listed Eternal (formerly Zomato), loses only about ₹3 per order. It is, in effect, at breakeven, and it is also the scale leader with 917 million orders. Zepto loses ~₹79; Instamart (Swiggy) loses ~₹85, and, unlike the other two, its per-order economics got worse in FY26.

So Zepto is in the middle: comfortably ahead of Instamart’s trajectory, but a long ₹76 per order behind the leader.

Zepto’s genuine edge: store productivity. It turns out to be the most orders per store of the three, about 562,000 a year, versus Blinkit’s 409,000, despite running half as many stores.

That efficiency is the most credible argument that it can close the gap to breakeven without simply pouring capital into more real estate.

And Now the Giants Are at the Gate

Amazon Now and Flipkart Minutes have entered.

The prospectus names both. They carry no separately disclosed quick-commerce numbers, which is exactly why they are not in the table above, but they are backed by Amazon and by Walmart-owned Flipkart, balance sheets that dwarf any pure-play.

Why a retail investor should care: their entry is precisely what makes the “we cut marketing” story fragile. In a four- or five-player land grab, deep-pocketed newcomers can reopen the discount war, and the spending discipline that flattered Zepto’s FY26 numbers is the first casualty, a risk that hangs over the entire Zepto IPO thesis.

One more comparison frames the valuation to come. Among the listed parents, only Eternal makes a profit, and the market values it at roughly 635 times earnings. Swiggy, like Zepto, loses money. There is, in short, no profitable, listed pure-play quick-commerce company in India against which to anchor Zepto’s price. That cuts both ways: enormous upside if Zepto becomes the profitable winner, and no floor if sentiment turns.

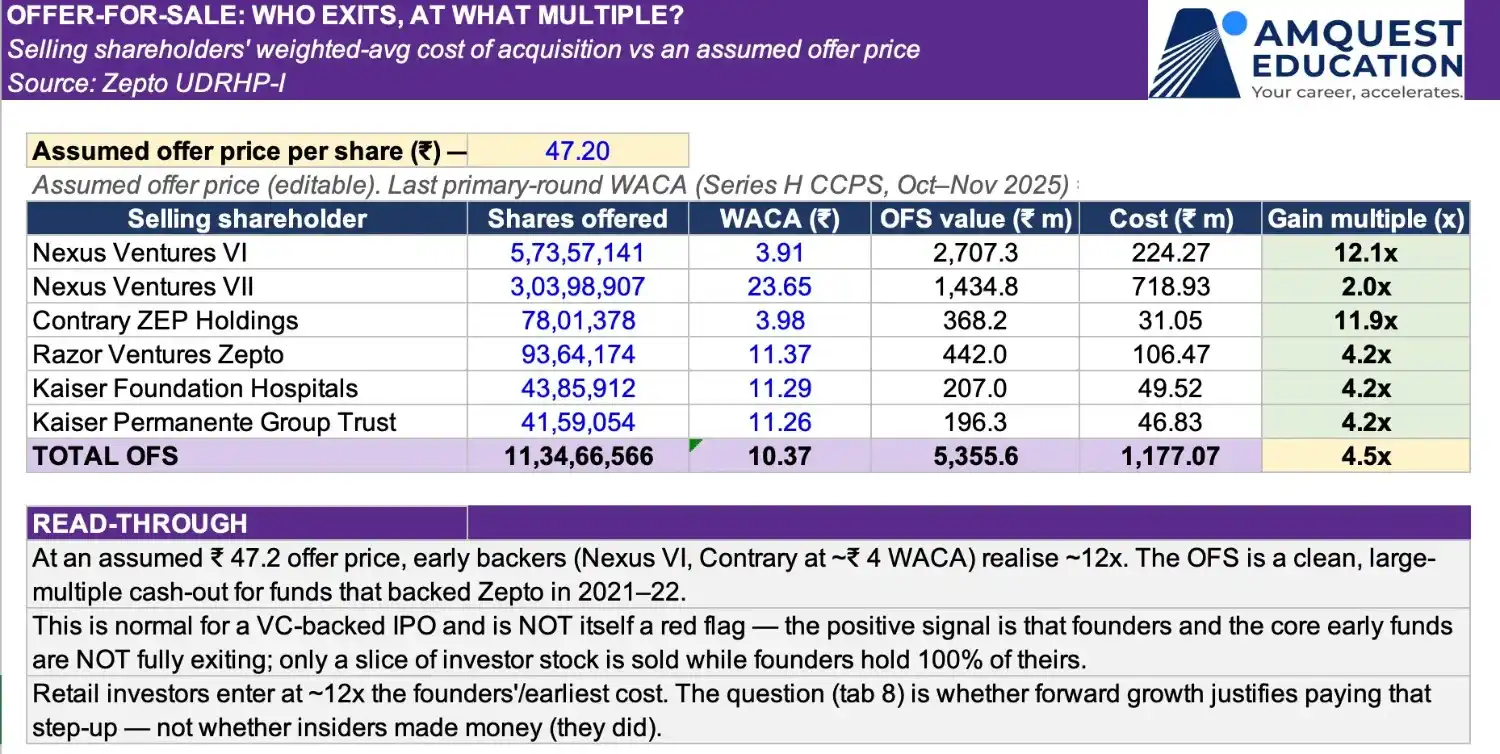

07 · WHO ACTUALLY GETS THE IPO MONEY

Who Actually Gets the Zepto IPO Money: A Fresh-Capital Raise on Top of an Investor Exit

Every IPO is two questions: how much new money goes into the company, and who is selling existing shares to cash out. The Zepto IPO answer is reassuring in one important respect and worth scrutinising in another.

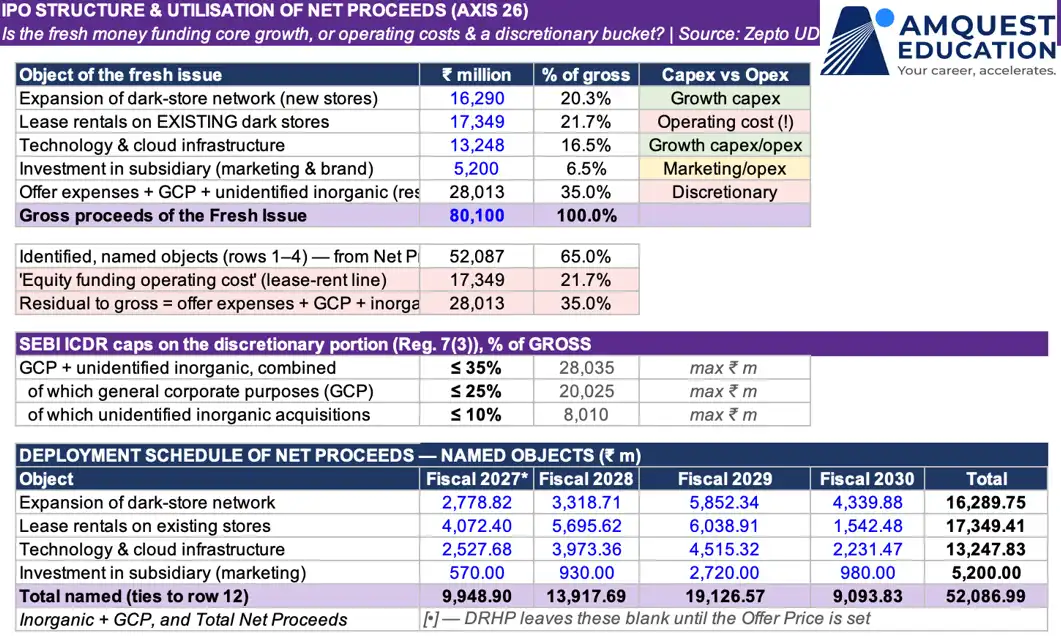

- Fresh issue, ₹80,100 million of brand-new shares, the proceeds of which go to the company to fund growth. This is the part that builds the business and forms the core of the Zepto IPO issue size.

- Offer for sale, 113,466,566 existing shares being sold by early investors. Crucially, every selling shareholder is a financial investor (Nexus, Contrary, Razorpay-linked and Kaiser entities). Not a single promoter or founder share is being sold. The founders are not cashing out, a genuine positive signal of alignment.

The early backers selling are doing very well: several acquired their stock at ₹3.91–₹23.65 a share, so even a modest IPO price is a multi-fold return. That is normal and fair; it is how venture capital recycles, but it does mean a meaningful slice of the offer is an exit for insiders rather than capital for the company.

What the New Money Is Earmarked For

Here is how the company plans to deploy the fresh proceeds from the Zepto IPO:

| Stated use of fresh proceeds | ₹ m | Comment |

|---|---|---|

| Rent on existing dark stores | 17,349 | Funding operating costs with equity, a flag |

| New dark stores | 16,290 | Genuine growth capex |

| Technology & cloud | 13,248 | Platform and infrastructure |

| Marketing (subsidiary) | 5,200 | Brand and acquisition |

| Named objects, subtotal | 52,087 | About two-thirds of the fresh issue |

| Offer expenses + general corporate + unidentified inorganic | ~28,013 | The discretionary remainder, SEBI caps apply |

Two things deserve a raised eyebrow. First, the single largest named use of IPO money, ₹17,349 million, is rent on dark stores the company already operates. Using permanent equity to pay a recurring operating bill is not what growth capital is supposed to do; it is closer to funding the burn.

Second, roughly a third of the proceeds fall into the loosely defined “general corporate purposes and future, unspecified acquisitions” bucket, right up against the regulatory ceiling for how much can be left unexplained. Both are legal and disclosed; both reduce how much of your money, as a Zepto IPO investor, is tied to a concrete growth plan.

08 · HOW THE SHAREHOLDING IS DESIGNED

Founders Own 2% Directly, and That Is Not the Red Flag It Looks Like

A first glance at the cap table alarms people: the two founders together hold under 2% of the company directly. But that is a feature of the structure, not a sign of absent skin in the game.

The bulk of the founders’ economic interest, around 18.5% in total, is held in family trusts: the Lazarus Trust (about 9.0%) on the Palicha side and the Vohra Trust (about 7.5%) on the Vohra side.

The wealth stays in the family; it is simply held one step removed. This shareholding structure is an important part of the Zepto IPO story for anyone weighing founder alignment.

The Number That Should Anchor Your Sense of Price

The last private round was struck at ₹37.74 a share.

The prospectus discloses the weighted-average cost of recent primary fund-raising (the Series H rounds of October–November 2025) as ₹37.74. On the company’s ~12.60 billion fully-diluted shares, that implies an equity value of roughly ₹475,645 million, about US$5.6 billion. Why it matters: that ~US$5.6 billion is a hard, prospectus-sourced anchor, below the ~US$7 billion often quoted in the press. If the IPO is priced above it, retail investors are buying in higher than the company’s own most recent private investors did, only months earlier. The eventual price band should be read against ₹37.74, and against this figure the Zepto IPO valuation will either look reasonable or stretched.

One more design choice to note: the employee stock-option pool is large enough to represent roughly 9% of the company fully diluted, and the exercise price was cut to almost nothing. That is great for retaining talent in a fierce hiring market, but it is a real future dilution and a recurring non-cash cost (₹5,569 million of share-based pay ran through FY26) that existing and incoming shareholders ultimately bear.

09 · GOVERNANCE FLAGS

The Disclosures That Deserve a Second Read

Most of Zepto’s governance is unremarkable for a fast-scaled startup. Three items, however, belong on any serious checklist before the Zepto IPO:

- A live regulatory matter against both founders. The Enforcement Directorate issued a summons to both founders in April 2026 in connection with the company’s “reverse flip,” the unwinding of its earlier overseas (Singapore) holding structure back into India, under foreign-exchange law. It is at an early stage and may come to nothing, but an open ED/FEMA inquiry naming the two key people is the single most material governance disclosure in the document.

- Key-person concentration. The entire thesis rests on two people still in their early twenties. There is no deep, proven bench disclosed beneath them. That is normal for a young company and a risk for a public one.

- Consumer-practice and gig-labour exposure. The company has faced a consumer-authority penalty over “dark pattern” interface practices (under challenge), and like all quick-commerce operators, it depends on a gig-worker fleet (about 221,667 active delivery partners, monthly average) whose classification and benefits are an evolving regulatory question.

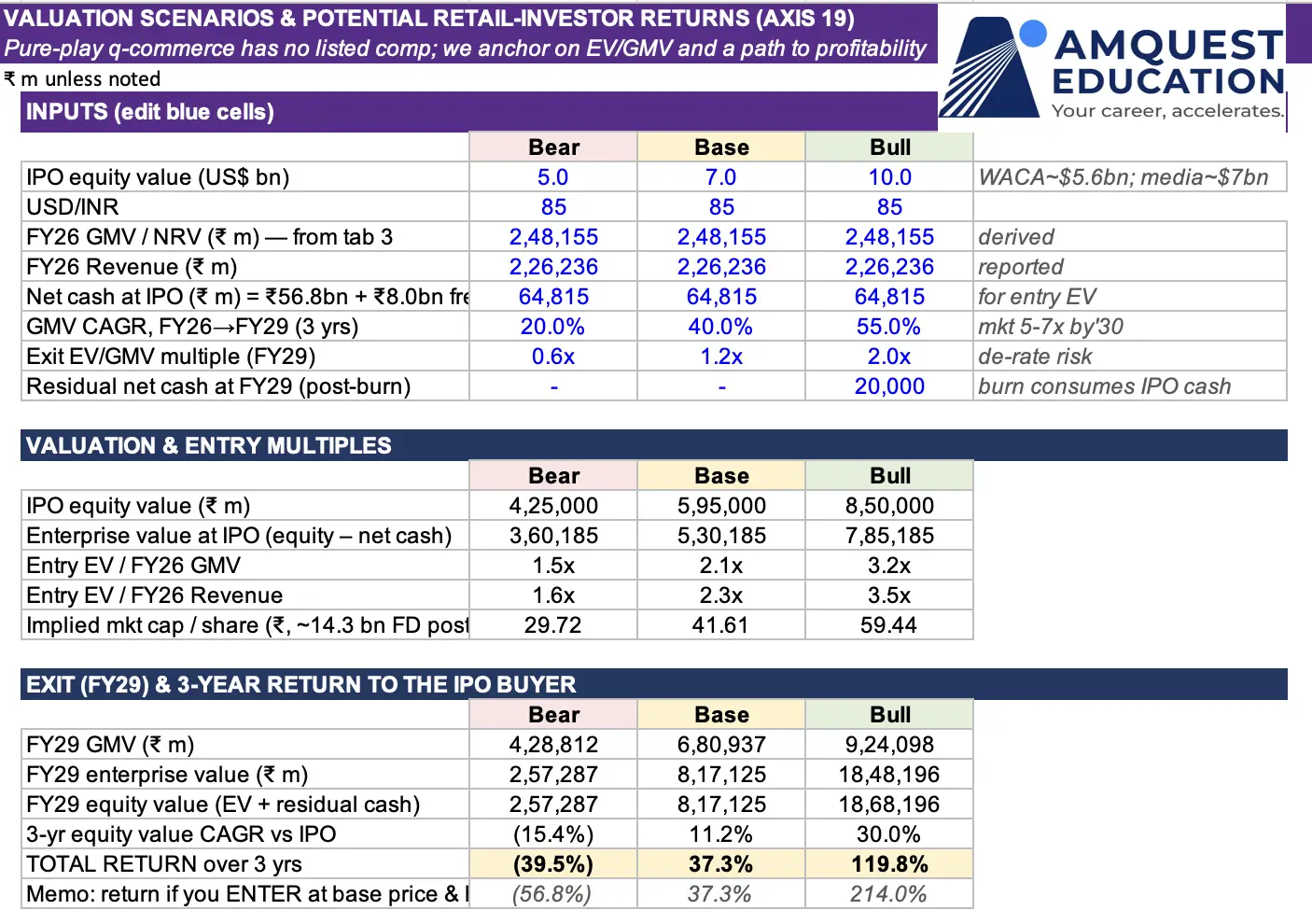

10 · THE VALUATION QUESTION

A Good Company at a Demanding Price

Because there is no profitable pure-play comp and Zepto itself loses money, you cannot value it on earnings. The honest approach is a scenario on the value of goods sold and the path to profit. Do that, and the entire return depends on one variable: the multiple the market is willing to put on the business when you eventually sell.

The arithmetic is unforgiving. At the kind of entry value implied around the last round and the press figures, the business is already priced at roughly two times the value of goods sold, a rich multiple for a company still losing ₹79 an order. In the model’s scenarios, an investor entering near the base case sees a wide spread of outcomes: a strong gain if Zepto compounds toward Blinkit-like economics and lists at a premium, and a painful loss, on the order of half your capital, if the market de-rates quick commerce or the price war reignites. The downside is not theoretical.

This is not a bad company. It is a good company at a price that already assumes years of flawless execution, and that tension is exactly what makes the Zepto IPO such a closely debated listing.

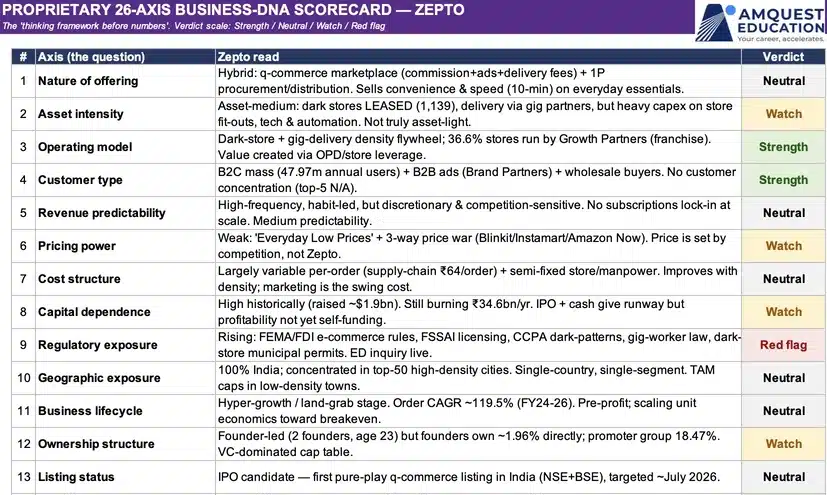

11 · THE BUSINESS-DNA SCORECARD

Twenty-Six Axes, Four Verdicts

The companion model scores Zepto across 26 dimensions of business quality, from revenue durability and unit economics to governance, capital allocation and valuation. The tally is the quickest summary of the whole investment case, and of the Zepto IPO as a whole:

| Strengths | Neutral | Watch items | Red flags |

|---|---|---|---|

| 6 | 5 | 11 | 4 |

The strengths are real: a category growing five-to-seven-fold this decade, a genuine scale position, the most productive stores in the field, and a fast-compounding advertising engine. But the centre of gravity is in “watch” and “red,” the unprofitability, the cash burn, the regulatory matter, the demanding entry price. A great story; an unfinished one.

Download the Zepto Financial Model, Research Report and the Investment Memo

12 · THE WATCH LIST

What a Careful Investor Tracks Before and After the Zepto IPO Price Band

- The price band against ₹37.74. How big a premium to the last private round are you being asked to pay in the Zepto IPO? The anchor-book demand from institutions on day one tells you what professional money thinks.

- Adjusted EBITDA per order, every quarter. Is the loss still shrinking, and is it shrinking on supply-chain and advertising, or only on marketing cuts that competition can reverse?

- Marketing spend per order. If it spikes back up, the FY26 “improvement” was a pre-IPO optimisation, not a structural turn.

- The gap to Blinkit. The leader is at breakeven and inside a profitable parent. Zepto closing that ~₹76-per-order gap is the bull case; the gap widening is the bear case.

- The ED matter, and runway. Progress on the FEMA inquiry, and with ~₹56.8 billion of cash plus the fresh issue against a ₹35 billion annual burn, roughly how many years before another raise is needed.

- Position sizing. Whatever the decision, this is a high-volatility, binary-outcome equity. It is the kind of holding that is sized to a loss you can absorb, not bet on as a sure thing.

- Zepto IPO issue size and listing timeline. Keep an eye on the official Zepto IPO issue size, the subscription numbers, and the listing schedule once the offer opens, since these details shape how much allotment retail investors actually receive.

The Verdict

A category leader-in-waiting with real strengths and a credible, if unproven, path to profit, offered at a price that already prices much of that success in. The most rational stance is engagement with discipline: judge it against the ₹37.74 anchor and the institutional anchor book, demand a margin of safety, and size any position to the genuine risk that quick commerce is a winner-take-most game in which Zepto is, today, the productive number two rather than the profitable number one. This verdict captures the central tension at the heart of the Zepto IPO.

Disclaimer

This article is an independent, educational analysis built from Zepto Limited’s draft prospectus. It is not investment advice, a recommendation, or an offer to buy or sell any security; the author is not your financial adviser. An IPO in a loss-making business carries a real risk of permanent capital loss. Read the final Red Herring Prospectus and consult a registered adviser before investing in the Zepto IPO. Figures may contain rounding; where the prospectus uses defined or non-GAAP terms, those definitions govern.