Investing is about combining assets to create a portfolio that meets client objectives, not just picking individual securities.

Diversification reduces risk without necessarily lowering expected return.

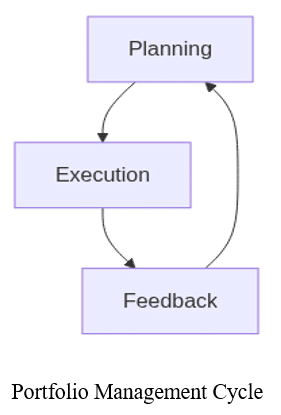

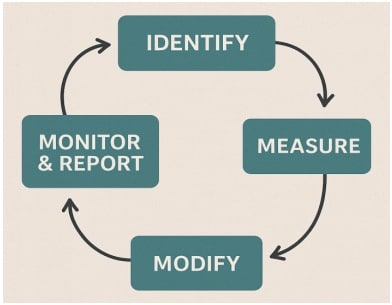

Portfolio Management Process

1. Planning: This step defines the investor’s objectives, risk tolerance, constraints, and creates an Investment Policy Statement (IPS). It sets the strategic asset allocation aligned with the client’s long-term goals.

2. Execution: The portfolio manager selects individual securities and constructs the portfolio based on the planned strategy. This includes implementing tactical asset allocation and using trading strategies to minimize costs.

3. Feedback: Involves ongoing monitoring of portfolio performance and client circumstances. Rebalancing and performance evaluation are performed regularly to ensure adherence to the IPS.

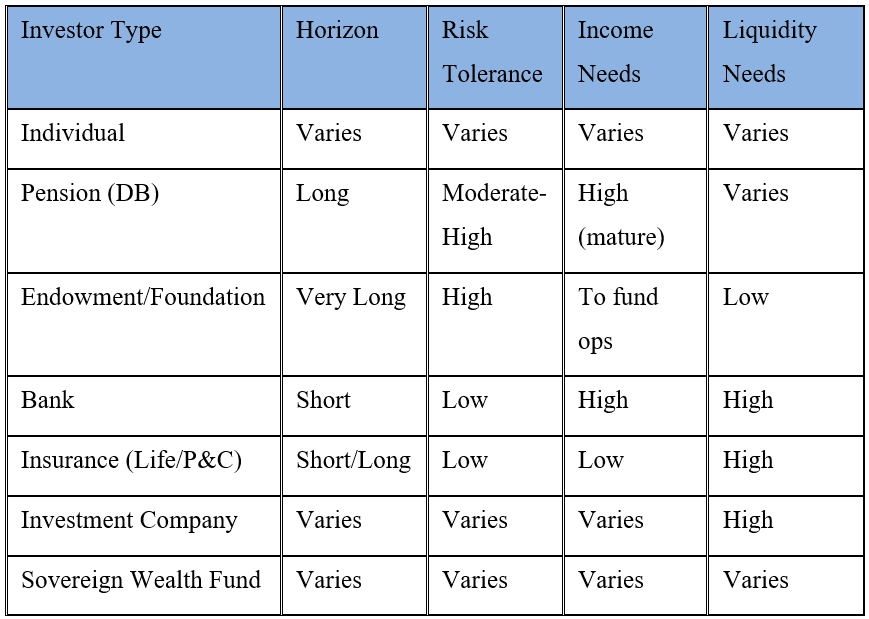

Types of Investors

Defined Benefit vs Defined Contribution Plans

DB Plan: Employer promises fixed benefit; employer bears investment risk.

DC Plan: Employer/employee contribute; employee bears investment risk.

2.Portfolio Risk & Return: Part I

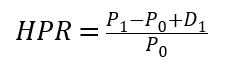

Major Return Measures

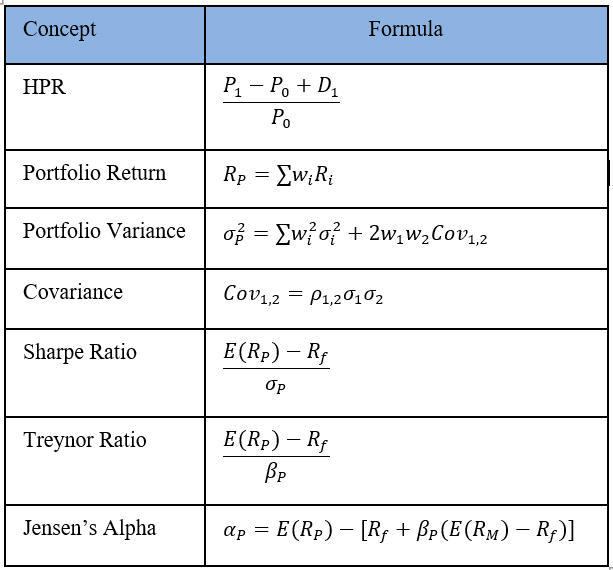

Holding Period Return (HPR):

Arithmetic Mean: Simple average return.

Geometric Mean: Compound average return.

Risk Measures

Variance : Average squared deviation from mean.

Standard Deviation : Square root of variance.

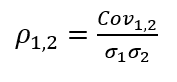

Covariance: Measure of how two assets move together.

Correlation :

Portfolio Risk (Two-Asset Portfolio)

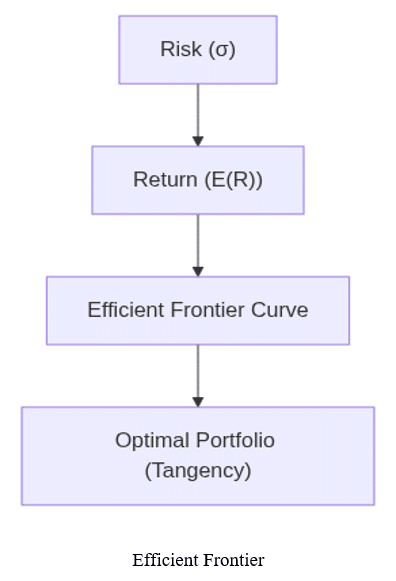

Efficient Frontier

Set of portfolios offering highest expected return for a given risk.

Optimal Portfolio: Tangency point with investor’s highest indifference curve.

3.Portfolio Risk & Return: Part II

Risk-Free and Risky Assets

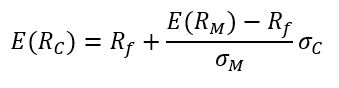

Capital Allocation Line (CAL): Combines risk-free asset and risky portfolio.

Capital Market Line (CML): CAL using the market portfolio as the risky asset.

Systematic vs. Unsystematic Risk

Systematic (Market) Risk: Cannot be diversified away.

Unsystematic (Unique) Risk: Can be reduced via diversification.

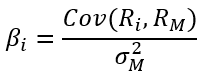

Beta

Measures sensitivity of asset returns to market returns.

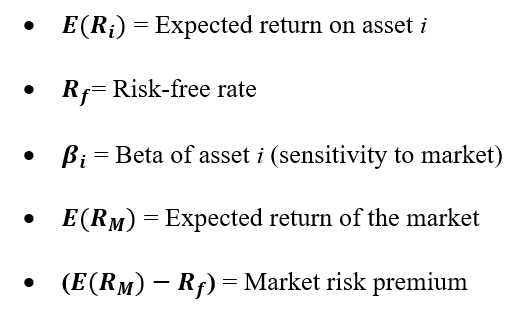

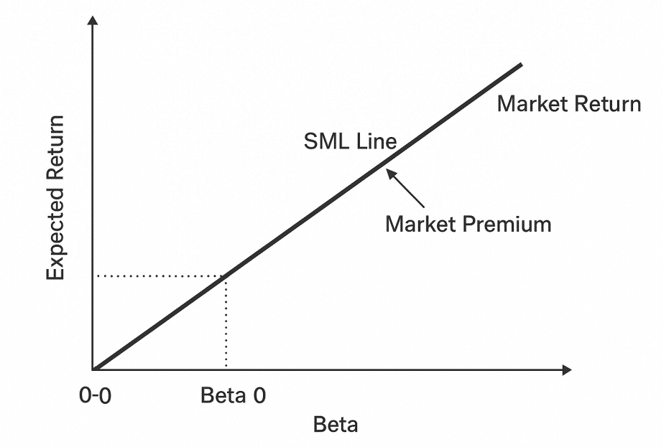

Security Market Line (SML) & CAPM

Interpretation: A higher beta means higher sensitivity to market movements and thus a higher required return. CAPM helps compare if a stock is overvalued or undervalued by comparing expected return vs. required return.

SML

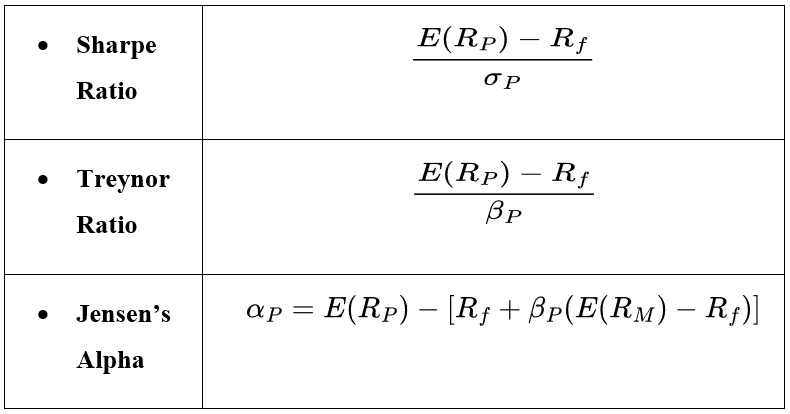

Risk-Adjusted Return Measures

4.Basics of Portfolio Planning & Construction

Investment Policy Statement (IPS)

Purpose: Road-map for managing investments.

Components: Objectives (risk/return), constraints (liquidity, time, taxes, legal, unique).

IPS Structure

Asset Allocation

Strategic: Long-term mix of asset classes.

Tactical: Short-term adjustments to exploit opportunities.

5.Behavioral Biases of Individuals

Cognitive Errors

Belief Perseverance: Conservatism, confirmation, representativeness, illusion of control, hindsight bias.

Loss aversion: The tendency to perceive losses as more painful than equivalent gains are pleasurable, leading individuals to strongly prefer avoiding losses over acquiring gains.

Overconfidence: The bias where a person’s subjective confidence in their judgments or abilities exceeds their objective accuracy, often resulting in excessive risk-taking.

Self-control bias: The tendency to prioritize short-term satisfaction over long-term goals, leading to difficulty in resisting immediate temptations (not directly in search, but widely recognized in behavioral finance).

Status quo bias: The preference to maintain one’s current situation or decisions, perceiving change as a potential loss and thus avoiding alternatives.

Endowment effect: The tendency to assign a higher value to objects simply because one owns them, regardless of their actual market value.

Regret aversion: The tendency to avoid making decisions or taking actions due to fear of future regret, often resulting in inaction or sub-optimal choices.