Learning Module 1: Introduction to Financial Statement Analysis

Overview

This module introduces the scope, purpose, and framework of financial statement analysis. It explains how analysts use financial reports to assess a company’s performance, financial position, and future prospects.

Objectives of Financial Statement Analysis

Evaluate profitability, risk, and financial health of a business

Support investment, credit, and valuation decisions

Use financial reports to assess past performance and predict future outcomes

Key Financial Statements

Financial Reporting Standards

IFRS and US GAAP govern preparation and presentation

Promote transparency, consistency, and comparability

The Analyst’s Approach to FSA

Understand the Business: Industry, strategy, risks

FSA supports decision-making for equity, debt, and business analysis

Requires understanding of financial reports and standards (IFRS/GAAP)

Notes, footnotes, and MD&A enhance transparency and interpretation

Suggested Practice

Match financial statements with decision types (e.g., credit vs equity)

Identify disclosures that affect earnings quality

Practice interpreting the four core statements together

Learning Module 2: Analyzing Income Statements

Overview

This module focuses on analyzing the income statement, which shows a company’s financial performance over a period. It explains the components of revenue, expenses, and profit, and how these affect profitability and valuation.

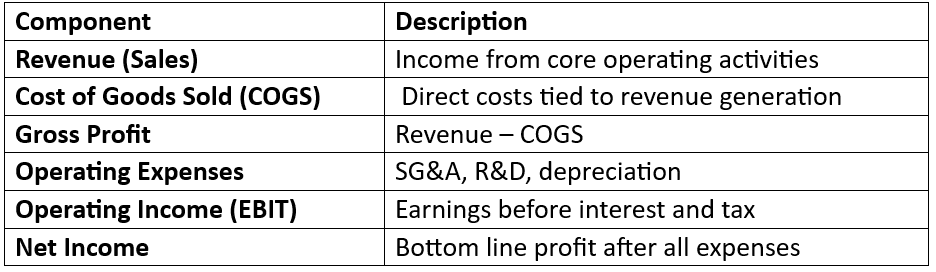

Structure of the Income Statement

Key Concepts

Accrual Basis: Revenues and expenses are recorded when earned/incurred, not when cash is exchanged

Multi-step vs. Single-step Statements:

Multi-step provides subtotals like gross and operating profit

Single-step aggregates all revenues and expenses

Earnings Quality Considerations

Recurring vs. Non-Recurring Items: Analysts adjust for one-time gains/losses

Operating vs. Non-Operating: Core vs. peripheral business activities

Earnings Management: Timing revenue/expense recognition to influence net income

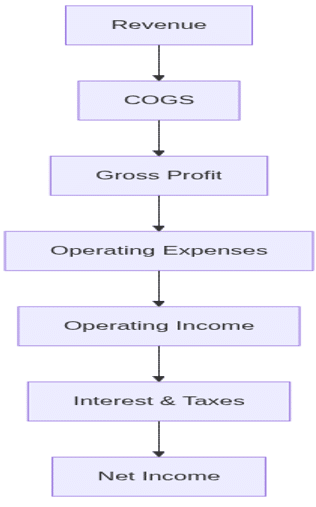

Visual: Income Statement Flow

Common Adjustments for Analysis

Exclude discontinued operations

Remove effects of changes in accounting estimates

Adjust for restructuring or impairment charges

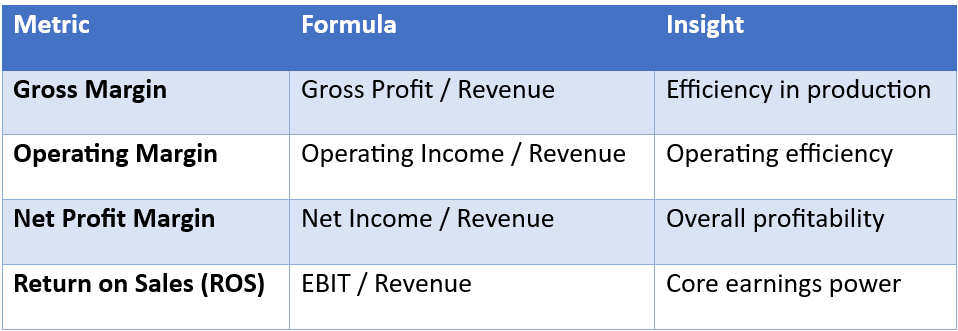

Profitability Metrics

Summary Points

Income statement shows revenues, expenses, and profitability

Adjust for unusual items to analyze sustainable earnings

Key margins reveal efficiency and financial performance

Suggested Practice

Identify and adjust for one-time items in sample statements

Calculate and interpret margin ratios

Compare operating vs. non-operating components in company reports

Learning Module 3: Analyzing Balance Sheets

Overview

This module explains the structure, components, and interpretation of the balance sheet. It provides insights into a company’s financial position at a point in time, including its assets, liabilities, and equity.

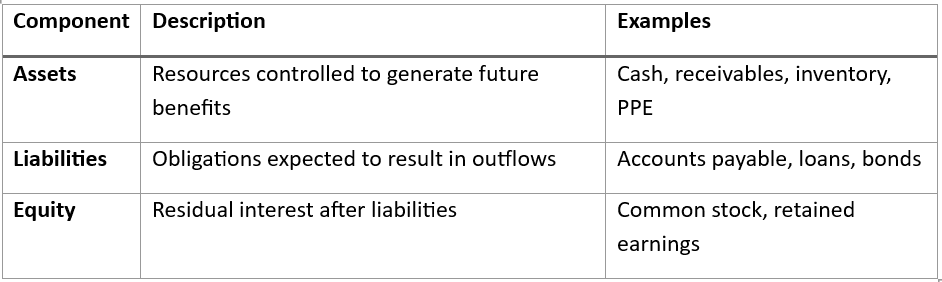

Purpose of the Balance Sheet

Shows the financial condition of a company

Presents the resources owned (assets) and claims (liabilities + equity)

Helps evaluate liquidity, solvency, and capital structure

Equation:

Assets = Liabilities + Equity

Current vs. Non-Current Items

Current: Expected to be settled/used within 12 months

Non-Current: Long-term in nature (e.g., PPE, long-term debt)

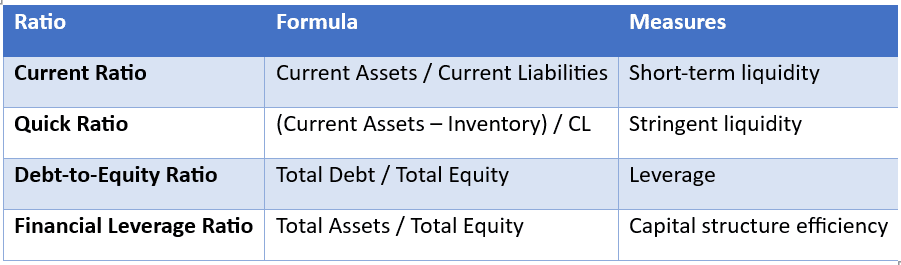

Capital Structure Mix: Debt vs equity financing implications

Summary Points

Balance sheet reveals financial position and capital structure

Segregates current and non-current items to assess liquidity and solvency

Key ratios provide insight into financial flexibility

Suggested Practice

Reconstruct balance sheet from transaction data

Calculate and interpret leverage and liquidity ratios

Overview

This module covers the structure and interpretation of the Cash Flow Statement, focusing on understanding how cash is generated and used in operating, investing, and financing activities.

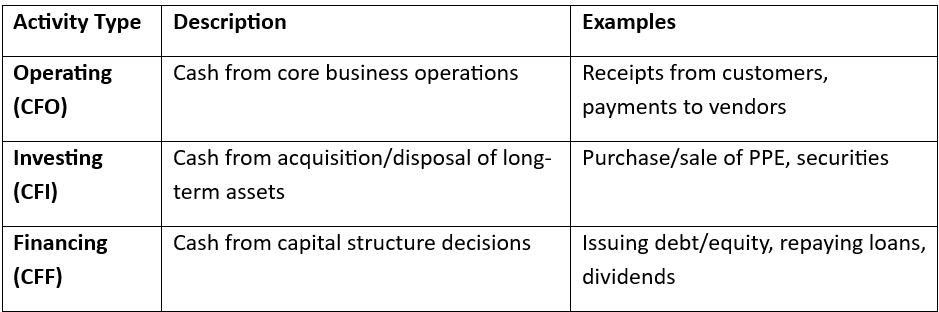

Purpose of Cash Flow Statement

Explains changes in cash and cash equivalents

Helps evaluate liquidity, solvency, and financial flexibility

Complements the income statement by showing actual cash movements

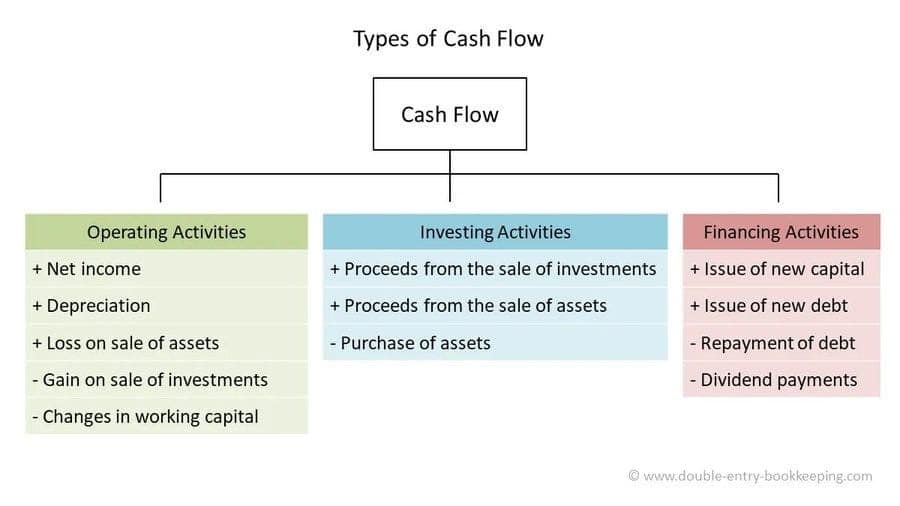

Subtract: Gains, Increase in current assets, Decrease in current liabilities

Analytical Uses

Assess quality of earnings (compare CFO to net income)

Determine sustainability of operations without external financing

Identify investment or financing trends

Summary Points

Cash flow statement clarifies actual inflows/outflows

Divided into operating, investing, and financing sections

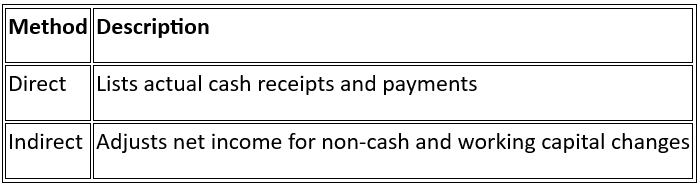

Indirect method adjusts net income to reflect cash reality

Suggested Practice

Classify cash flows by activity type

Reconcile indirect CFO from net income

Compare CFO to net income and evaluate quality of earnings

Learning Module 5: Analyzing Cash Flow Statements II

Overview

This module builds on the understanding of the cash flow statement by diving deeper into cash flow analysis, interpretation of cash flow patterns, and how to assess a firm’s cash-generating ability and sustainability.

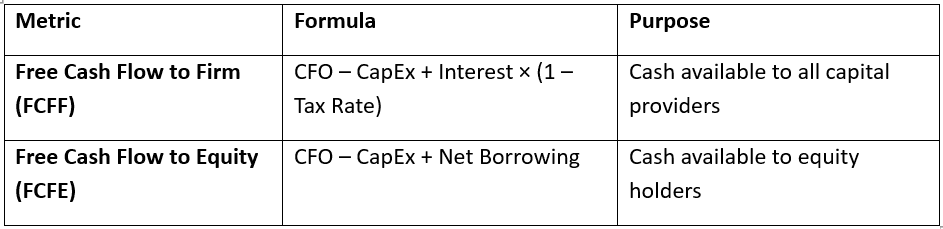

Free cash flows assess cash available for reinvestment or distribution

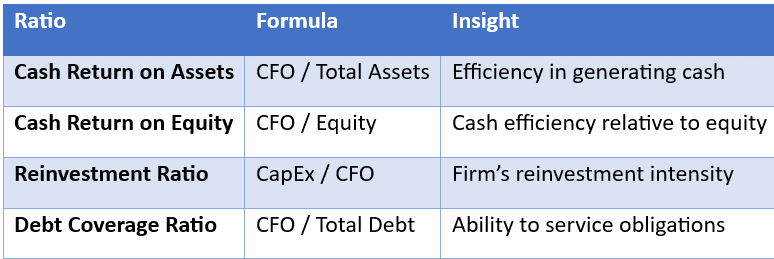

Ratios enhance interpretation of cash generation vs capital structure

Suggested Practice

Calculate FCFF/FCFE from sample data

Use cash-based ratios to compare peer performance

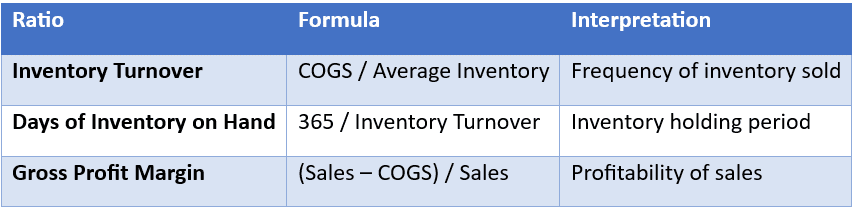

Learning Module 6: Analysis of Inventories

Overview

This module focuses on inventory accounting methods and their impact on financial statements. It helps analysts assess cost flows, earnings quality, and inventory management efficiency.

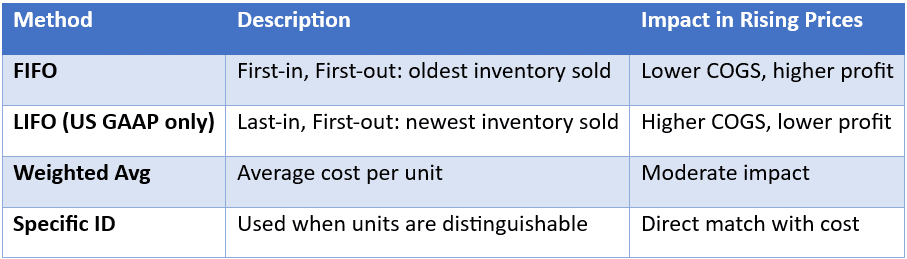

Inventory Accounting Methods

IFRS prohibits LIFO

Inventory’s Financial Statement Impact

Affects COGS, gross profit, net income, taxes, inventory balances, and ratios

Inventory valuation errors distort both income statement and balance sheet

Inventory Ratios

Higher turnover and lower days indicate efficiency, but may also signal stockouts.

LIFO Reserve & Comparability

LIFO Reserve = FIFO Inventory – LIFO Inventory

Used to adjust LIFO firms to FIFO for comparability

FIFO results in higher income during inflationary periods

LIFO Reserve enables cross-firm comparisons

Suggested Practice

Convert LIFO to FIFO using LIFO reserve

Analyze turnover and inventory days across firms

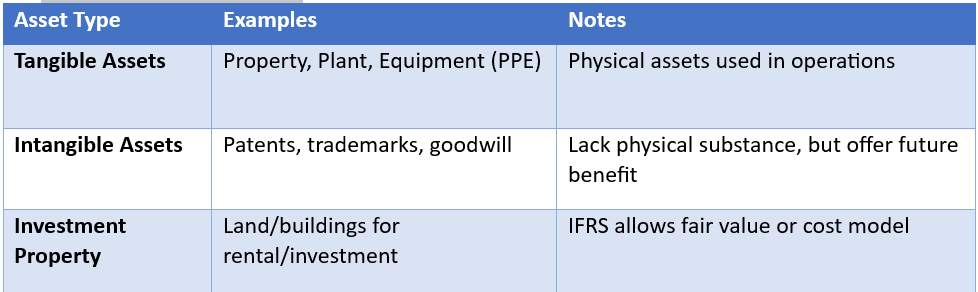

Learning Module 7: Analysis of Long-term Assets

Overview

This module covers the accounting and analysis of long-term (non-current) assets, including tangible, intangible, and investment assets. It explores measurement, depreciation, impairment, and revaluation effects on financial statements.

Types of Long-Term Assets

Measurement Models

Depreciation and Amortization

Depreciation: Allocation of cost of tangible assets over useful life

Amortization: Same for intangible assets (excluding indefinite-lived like goodwill)

Common methods:

Straight-Line: Equal expense each period

Declining Balance: Accelerated (higher earlier)

Units of Production: Based on output/use

Impairment of Long-Term Assets

Triggered by decline in asset’s recoverable value

IFRS: Compare carrying amount vs recoverable amount (higher of value in use or fair value – cost to sell)

US GAAP: Compare carrying amount to undiscounted future cash flows

Loss = Carrying amount – Recoverable amount (if impaired)

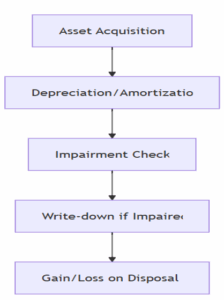

Derecognition

Occurs on sale, disposal, or permanent withdrawal of asset

Gain/Loss = Proceeds – Carrying amount

Visual: Asset Lifecycle and Effects

Impact on Financial Statements

Affects net income, asset values, equity, and ratios

Choice of depreciation method impacts timing of expense recognition

Summary Points

Long-term assets are critical to operations and valuation

IFRS allows more flexibility (revaluation) than US GAAP

Impairments reduce asset values and net income

Analysts adjust for depreciation methods and revaluations in comparisons

Suggested Practice

Compare asset valuation under cost vs revaluation model

Recalculate depreciation using different methods

Analyze impairment effect on profitability and asset turnover

Learning Module 8: Topics in Long-Term Liabilities and Equity

Overview

This module explains the classification, measurement, and analysis of long-term liabilities and equity, including bond issuance, leases, stockholders’ equity, and how these affect capital structure and financial performance.

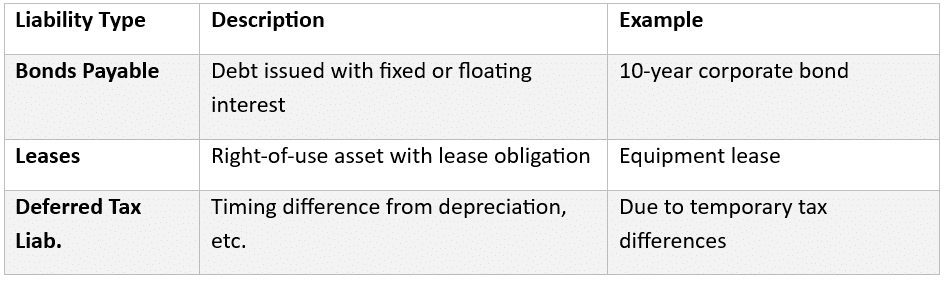

Long-Term Liabilities

Measurement: Recorded at present value of future payments

Lease Accounting

All leases (except short-term or low-value) are capitalized

Recognize Right-of-Use Asset and Lease Liability

Impact:

Higher assets and liabilities

Higher EBITDA (lease expense split into depreciation + interest)

Bonds and Interest Recognition

Bonds can be issued at par, premium, or discount

Interest Expense = Carrying Value × Market Rate

Difference between coupon and interest expense = Amortization of premium/discount

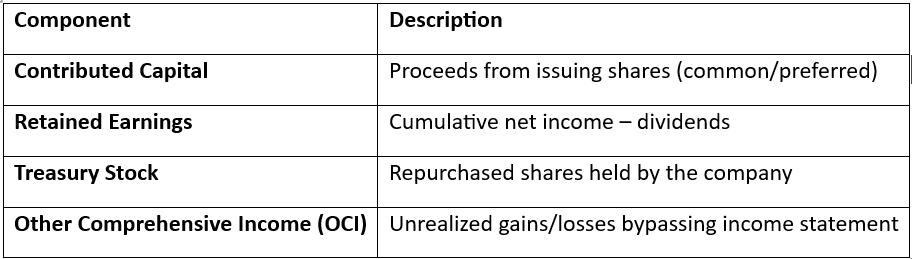

Equity Section Components

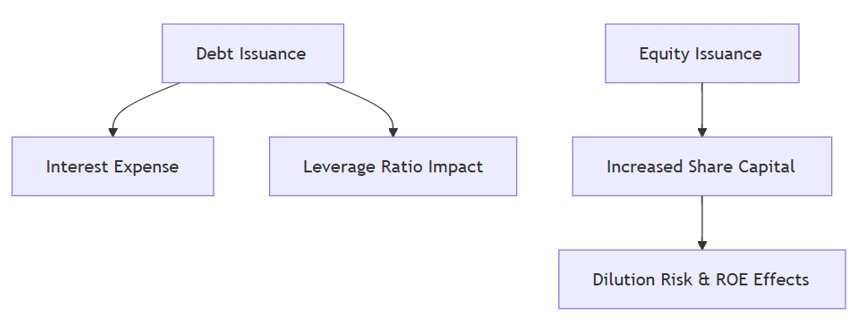

Visual: Capital Structure & Effects (Mermaid)

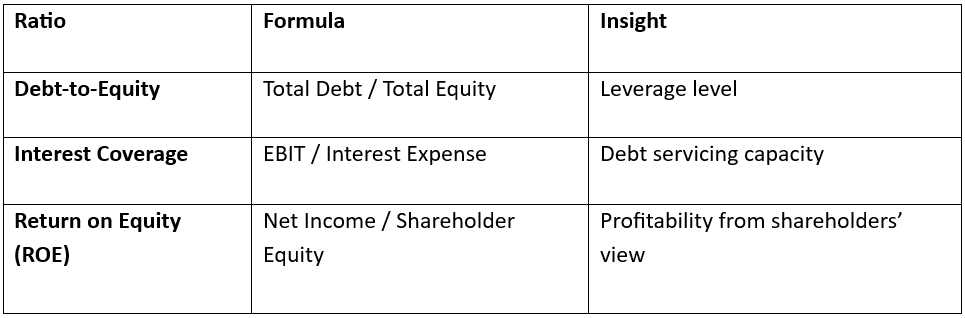

Key Ratios

Summary Points

Long-term liabilities increase leverage but can enhance returns

Leases and bonds impact both income and balance sheet differently

Equity includes both paid-in capital and retained earnings

Analysts track capital structure to assess risk and return

Suggested Practice

Analyze lease vs purchase impact on financials

Adjust ROE for share buybacks and new issuance

Interpret trends in debt and equity funding strategies

Learning Module 9: Analysis of Income Taxes

Overview

This module explains how income tax expense is recognized and analyzed in financial reporting. It focuses on temporary differences, deferred tax assets and liabilities, and their implications for evaluating earnings quality and financial health.

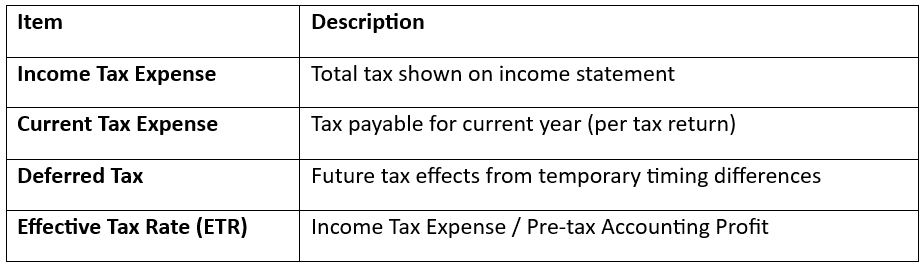

Components of Tax Reporting

Temporary vs. Permanent Differences

Temporary Differences: Cause deferred tax items; reverse over time

Depreciation methods (accounting vs tax)

Warranty expenses, bad debt provisions

Permanent Differences: Do not reverse; affect ETR but not deferred tax

Fines, tax-exempt income

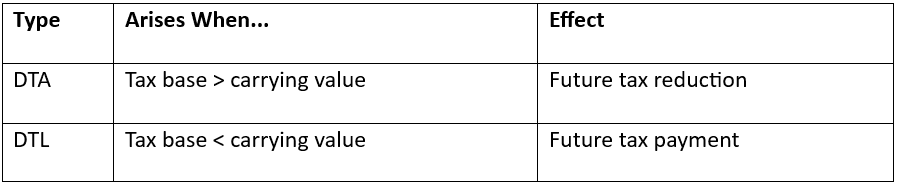

Deferred Tax Assets (DTA) and Liabilities (DTL)

DTA is recognized only if realization is probable

Valuation Allowance (US GAAP)

Applied to reduce DTA if future tax benefit unlikely

Affects net income and signals doubt about profitability

Analytical Implications

Rising DTLs may signal future tax cash outflows

Changes in tax laws affect valuation of deferred tax balances

Analysts adjust for one-time tax effects (e.g., changes in rate, reversals)

Summary Points

Tax expense has current and deferred components

Temporary differences lead to deferred tax items

DTA realization requires future taxable income

ETR analysis reveals discrepancies between accounting and tax reporting

Suggested Practice

Classify tax differences as permanent or temporary

Reconstruct tax expense from DTA/DTL changes

Interpret implications of valuation allowance and ETR movement

Learning Module 10: Financial Reporting Quality

Overview

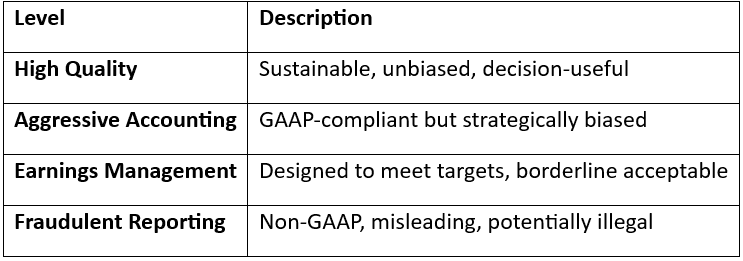

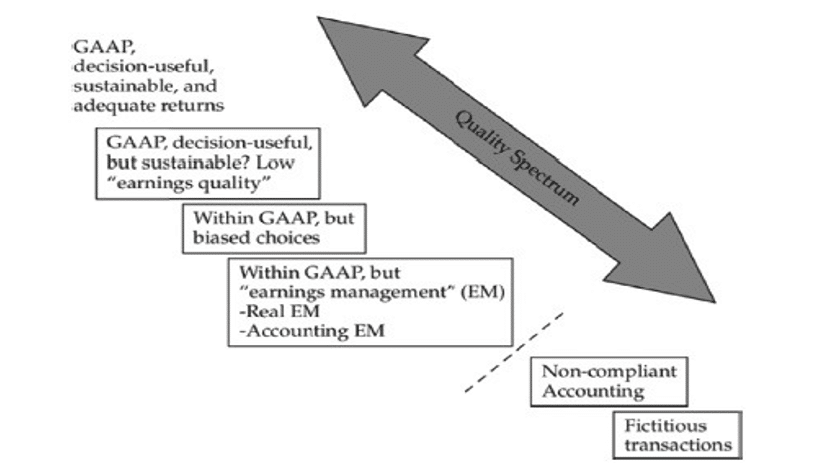

This module explores the concept of financial reporting quality, distinguishing between high- and low-quality reporting, and identifying earnings manipulation techniques that affect decision usefulness.

Two Dimensions of Financial Reporting Quality

Decision-Usefulness: Is the information relevant and faithfully represented?

Earnings Quality: Are reported earnings sustainable and unbiased?

Characteristics of High-Quality Reporting

Transparent: Clear and detailed disclosures

Comprehensive: Includes all material transactions

Consistent: Over time and aligned with economic reality

Low-quality reporting distorts financial position and performance

Analysts use consistency, transparency, and earnings persistence to evaluate quality

Suggested Practice

Identify red flags in sample income statements

Analyze cash flow vs net income to detect manipulation

Rank earnings quality across peer companies using real disclosures

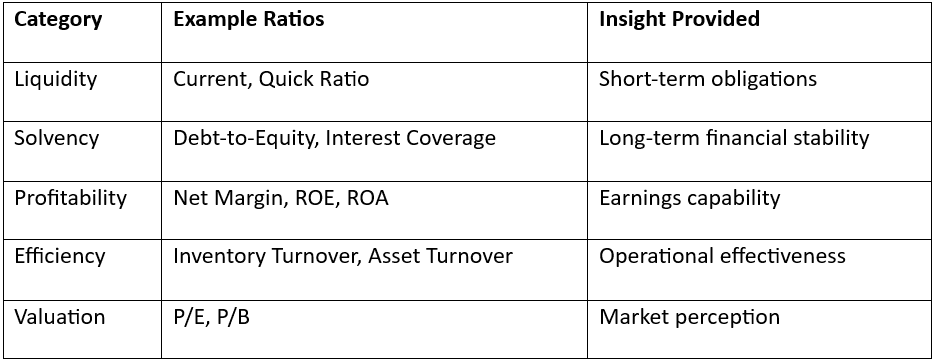

Learning Module 11: Financial Analysis Techniques

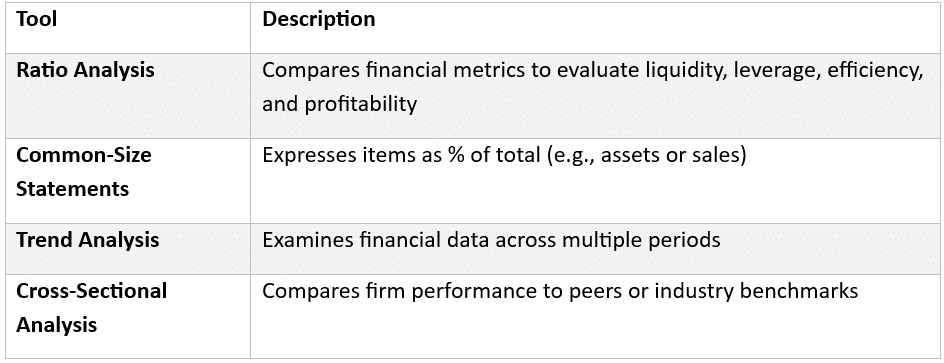

Overview

This module outlines key tools and techniques used to analyze financial statements. It includes ratio analysis, common-size and trend analysis, and how these help evaluate performance, risk, and financial health.

Ratios affected by seasonality, inflation, or timing differences

Interpretation requires context and comparison

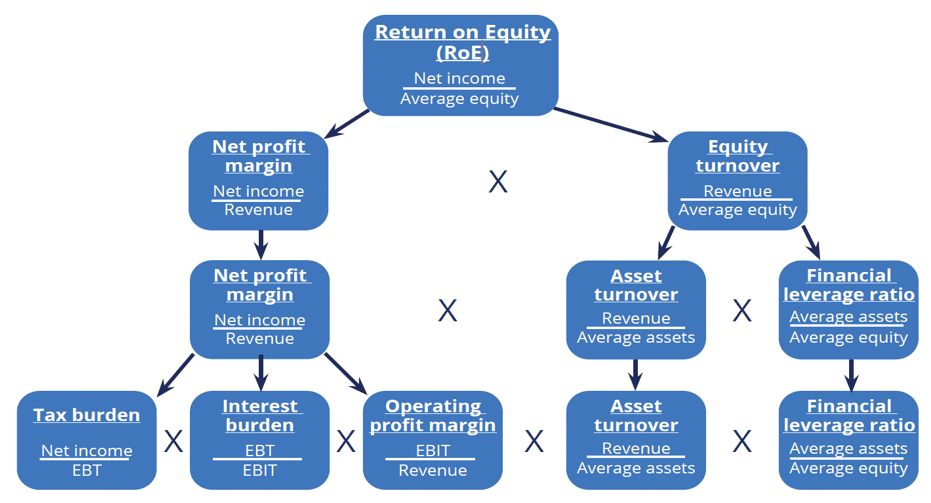

Summary Points

Financial analysis evaluates performance and risk using structured tools

Ratio and common-size analysis provide insights into business health

DuPont breaks down ROE into actionable drivers

Suggested Practice

Decompose ROE for 3 companies using DuPont

Compare trend and common-size statements across years

Evaluate peer group financial ratios and identify outliers

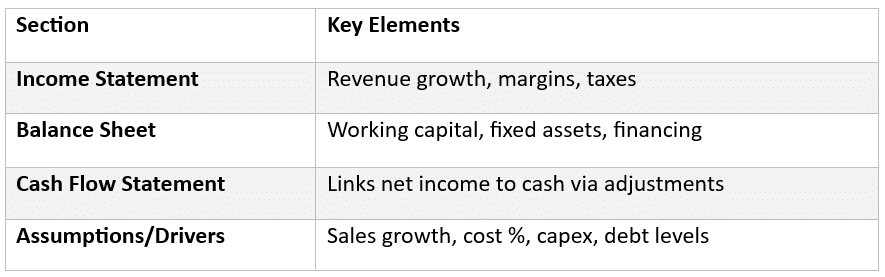

Learning Module 12: Introduction to Financial Statement Modeling

Overview

This module introduces the basics of financial modeling, focusing on how financial statements can be forecasted and linked to estimate a company’s future performance using assumptions and historical data.

Purpose of Financial Modeling

Project future income, cash flow, and balance sheet items

Support valuation, budgeting, and decision-making

Evaluate impact of strategic or macro assumptions on financials