Definition: A derivative is a financial contract whose value is based on (derived from) the value of an underlying asset, rate, or index (e.g., stocks, bonds, commodities, currencies, interest rates, credit, or even weather).

Key Features of Derivatives

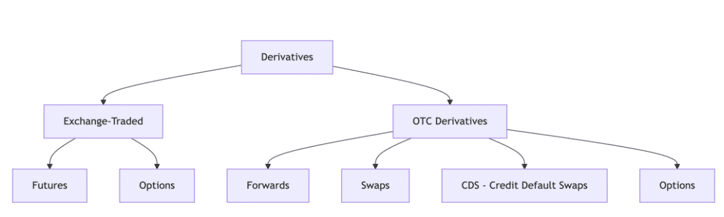

2. Types of Derivative Markets

Diagram: Market Structure

3. Types of Derivatives

1.Forward Commitments

Forwards: Private agreement to buy/sell an asset at a set price in the future.

Futures: Standardized, exchange-traded forwards with daily settlement.

Swaps: Agreements to exchange cash flows (e.g., fixed for floating interest).

2.Contingent Claims

Options: Right (not obligation) to buy (call) or sell (put) at a set price.

Credit Derivatives: E.g., Credit Default Swaps (CDS) to transfer credit risk.

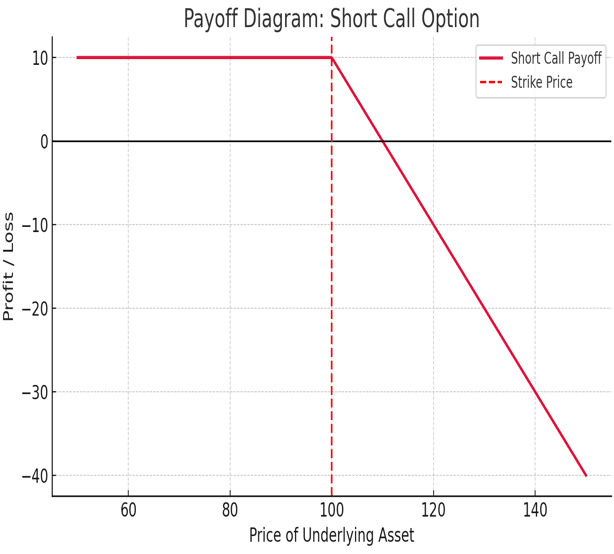

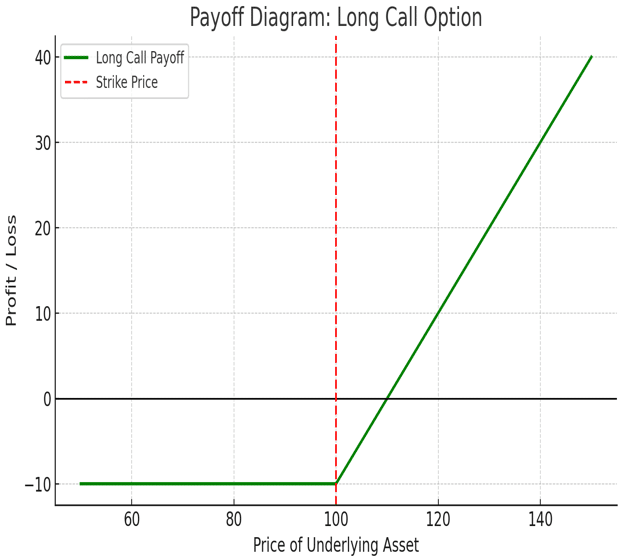

Payoff Diagram – Long and Short Call Option

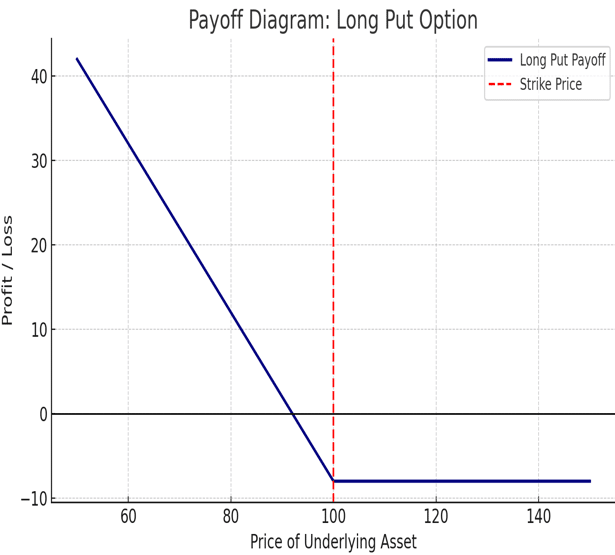

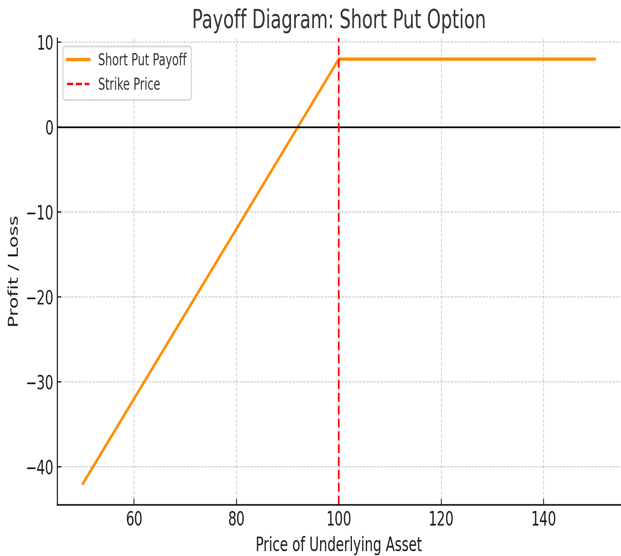

Payoff Diagram – Long and Short Put Option

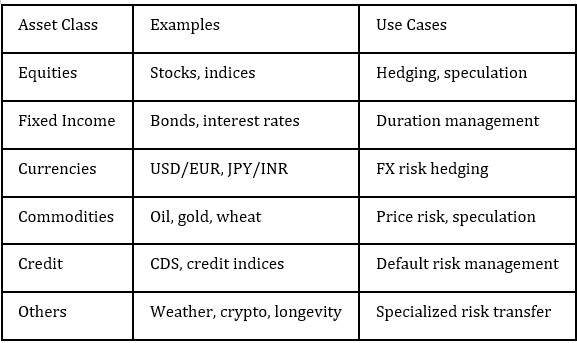

4.Derivative Underlyings

5.Benefits & Risks of Derivatives

Benefits

Risk Management: Hedge against price/interest/currency risks.

Price Discovery: Reveal expectations of future prices.

Operational Efficiency: Lower transaction costs, leverage, short selling.

Risks

Leverage Risk: Small price changes can lead to large gains/losses.

Basis Risk: Imperfect correlation with underlying.

Liquidity Risk: Some contracts may be hard to exit.

Counterparty Risk: Risk of other party default (mainly OTC).

Systemic Risk: Excessive use can threaten financial stability.

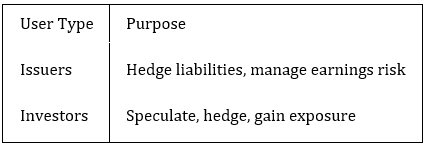

6.How Derivatives Are Used

7. Arbitrage, Replication & Cost of Carry

Arbitrage: Risk-free profit from price differences.

Replication: Constructing a derivative payoff using underlying + cash.

Cost of Carry: Net cost/benefit of holding an asset (storage, interest, dividends).

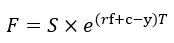

Formula: Forward Price=

Where:

F = Forward price

S = Spot price

rf = Risk-free rate

c = Storage cost

y = Yield

T = Time to maturity

8.Pricing and Valuation

Forwards & Futures

Value at Inception: Zero (no money exchanged).

Value During Life: Difference between current forward price and contract price, discounted at risk-free rate.

It shows how to calculate the current value of a forward contract (to the long position) by adjusting for carrying costs and benefits.

Swaps

Value: Present value of net future cash flows.

Options

9.Option Replication & Put-Call Parity

Put-Call Parity Formula:

Where:

C= Call price

P= Put price

PV(X) = Present value of strike price

S = Spot price

10.Binomial Option Pricing Model

Step 1: Assume two possible outcomes for the underlying price (up/down).

Step 2: Calculate option payoffs in each scenario.

Step 3: Use risk-neutral probabilities to discount expected payoff.

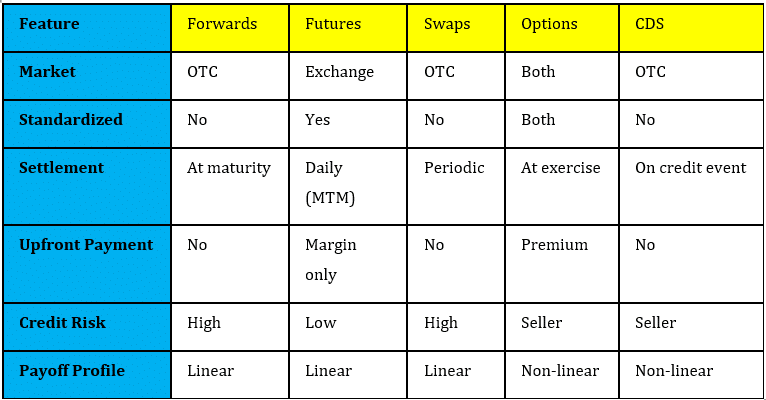

11.Summary Table: Derivative Contract Features

Derivatives are contracts based on other assets, used for managing risk or seeking profit. They come in several types, each with its own features, uses, and risks.

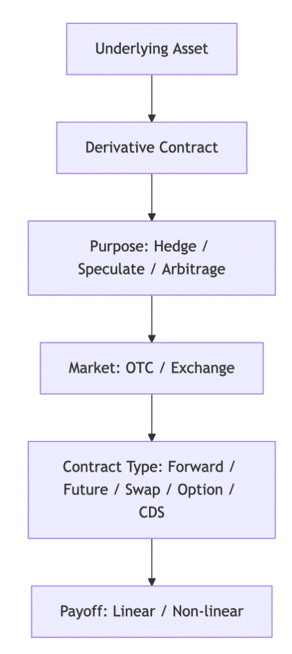

12.Visual Summary: Derivatives Landscape

Tips for Studying Derivatives

– Practice drawing payoff diagrams for calls, puts, forwards, and swaps. – Memorize key pricing formulas (cost of carry, put–call parity). – Understand differences: forwards vs. futures, swaps vs. forwards. – Focus on replication strategies and arbitrage principles. – Work through end-of-chapter questions to strengthen application.